Whether you need money to improve your home or cover a gap in employment, one way to obtain it fast and easily is with a personal loan.

What's more, personal loans are often less expensive and offer more favorable terms than other ways of borrowing money.

Denying yourself the opportunity of a personal loan not only means you deny yourself the possibility of getting your wants or needs met in the time frame that serves your circumstances. It could also have consequences far more dire.

For example, you may opt for an alternative means to obtain that wanted or needed money that costs you more and has stricter terms and more severe consequences should you default on repayment.

Alternatively, you may forego purchases that could improve your quality of life or, even, protect your health and safety.

By the end of this article, you'll understand the opportunity personal loans offer, the benefits and risks they pose, how to decide whether a personal loan is right for you and how to go about getting one.

What Are Personal Loans?

A personal loan is money you borrow from a credit union or other lender that you pay back in installments, or fixed monthly payments.

How Do Personal Loans Work?

All personal loans, no matter the lender, are comprised of several factors:

- Principal - The amount of money that you borrow

- Interest - The main "cost" for the loan, expressed as a percentage of the principal

- APR - The total cost for the loan, made up of the interest rate and any other ongoing fees associated with the loan

- Installment period - The amount of time you have to pay back the loan, including interest

- Monthly payment - The minimum amount you must pay each month toward repayment of the loan, divided amongst principal and interest according to the terms of the loan

A typical installment period for a personal loan is two to seven years, and a typical Annual Percentage Rate (APR) is 6%-36%, as of this Summer 2020 writing.

How to Qualify for a Personal Loan

Most lenders base eligibility for a personal loan on several of the same basic factors.

Credit score

Your credit score is a numerical encapsulation of your creditworthiness to lenders based on a set of factors, such as your current lines of credit and credit limits and the size of your current balances.

There are a few different scoring methods and entities, and different lenders use different ones in their assessments of applications, though they all use similar criteria.

Many lenders have strict rules around credit score ranges that do or don't qualify for certain loans and their interest rates and terms.

Income

Lenders want to make sure you can repay your loan according to the repayment terms of your loan agreement.

Your income is obviously a key factor in making this assessment. One way to improve your creditworthiness to lenders is to increase your income.

Consider taking on a second job or a part-time job in order to show a larger income on your personal loan application.

Credit report

Your credit report gives lenders more insight into the factors that influence your credit score.

If your credit score is too low to get the personal loan you want, look up your credit reports with the three major agencies (Equifax, Experian and Transunion) to see what issue, exactly, is pulling down your score.

You can look up your credit report from each of the three agencies once per year for free at annualcreditreport.com.

Beware of other websites claiming free credit reports that end up charging you money after all.

In some case, you may find an error negatively impacting your credit score, in which case you can contact the particular agency with proof of the error to correct on your credit report.

A month or so after a change occurs to your credit report, that change is reflected in your credit score.

Lenders also look for red flags in credit reports that tell them not to lend to a particular applicant, such as bankruptcies, foreclosures, delinquent payments and collection accounts.

Note: One key factor most lenders will consider when examining these criteria is your debt-to-income ratio. This metric shows lenders how financially stretched you are already and gives them a reasonable idea of how easily you'll be able to meet your repayment obligations to them with your current income and considering your other current obligations.

Be aware, as well, that every time a lender looks up your credit report, it impacts your credit score. You can significantly reduce this impact, however, by consolidating all these queries to a short period of time.

In other words, submit all your personal-loan applications within a short frame of time so that their successive credit report inquiries won't successively damage your credit score and, consequently, apparent creditworthiness.

You can qualify for a personal loan with less-than-perfect criteria, but you should expect your loan terms, such as interest rate, payment size, payment term, loan limit and fees, to differ accordingly.

Similarly, if you can't qualify for an unsecured loan, which requires no collateral, you may qualify for a secured loan, which does, or a co-signed loan, which requires a second person to take responsibility with you for the loan.

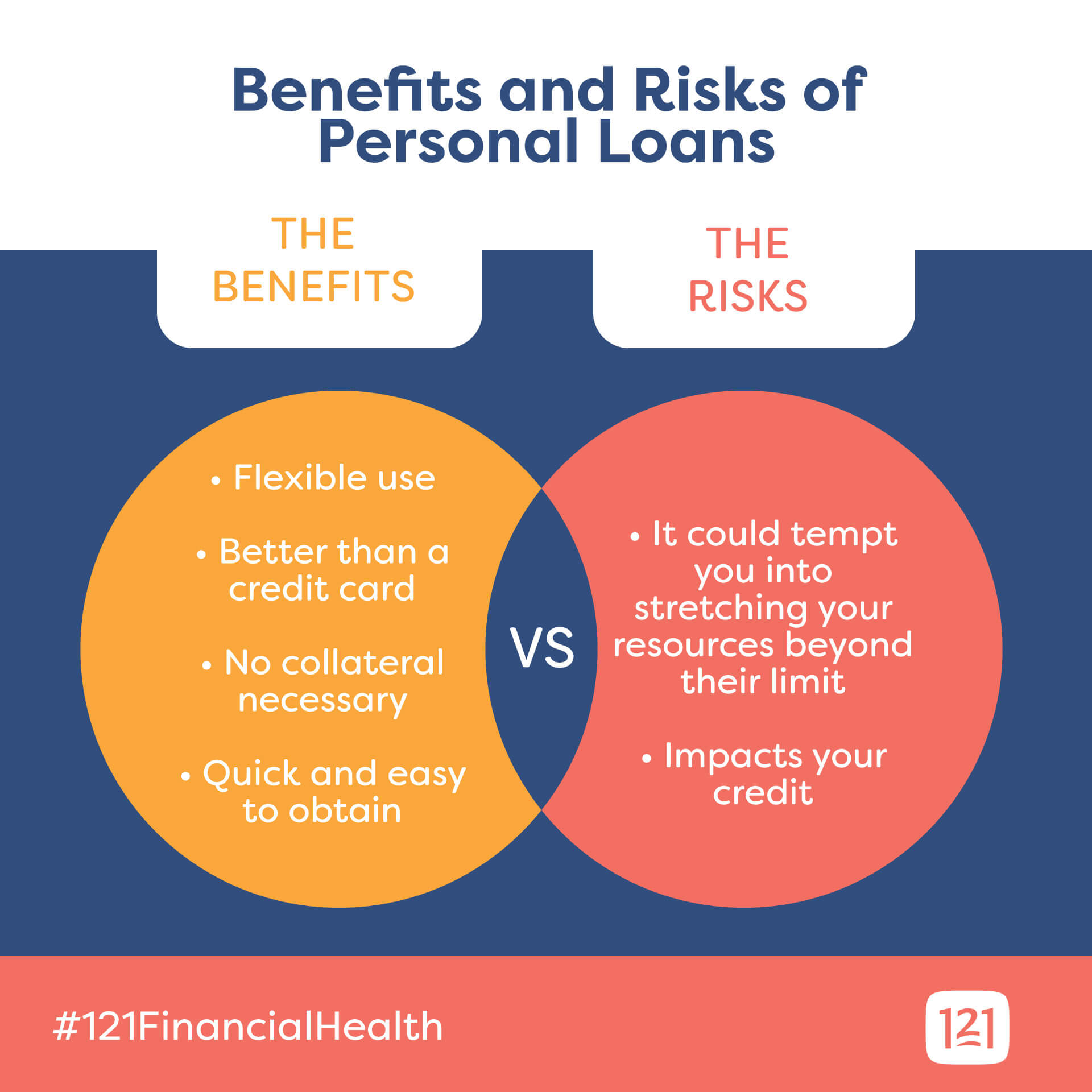

Benefits and Risks of Personal Loans

Like all financial instruments, while a personal loan does have its advantages, it also can have its risks.

Therefore, to make sure a personal loan is right for you and that your decision to get one won't have unintended negative consequences, make sure to be aware of all the risks as well as the benefits of personal loans before you follow through with one.

Benefits

Personal loans offer many advantages over and above other common options for accessing money or credit.

- Use for any reason - Whereas with a mortgage, student or car loan, for example, you can only use the money you borrow for a specified purpose, a personal loan allows "flexible use," meaning you can use it for any purpose whatsoever. That said, some lenders may impose certain restrictions on how you can spend the money, such as prohibiting you from applying it to education expenses.

Just some of the ways you may use a personal loan include to:

- Make home repairs or improvements

- Cover your needs during a gap in employment

- Start a new business or cover small business expenses

- Fund a child's education

- Cover an emergency medical need or pay an expensive medical bill

- Take the family for a vacation

- Pay for a wedding, honeymoon, divorce or funeral

- Buy holiday gifts

- Purchase home furniture or an appliance

- Consolidate debt

- Repay friends and family

- Finance moving costs

- Better than a credit card - Unless you're getting a promotional credit card rate, personal loans typically have lower APRs than credit cards. They also tend to have higher borrowing limits. For this reason, consolidating debt from multiple credit cards into a single personal loan is often a wise strategy for paying down that debt easier and for cheaper.

- No collateral necessary - Most personal loans are unsecured, meaning you don't have to put up any collateral in order to receive one. You can, however, find secured loans, and if you choose to take one, you can pay less over the life of the loan than you would for an unsecured loan (all else being equal,) but you could lose the asset you borrowed the money to purchase if you default on the loan.

- Quick and easy - Unlike other debt instruments that could take days, weeks or, even, months to obtain and may involve a mountain of paperwork, personal loans are relatively easy to apply for, and you could have your money the very next day.

Risks

Just because a personal loan may be available to you, it doesn't mean you should automatically take advantage of it.

First, there are certain precautions you should take into consideration.

- Overextending yourself - Like a credit card, the relative ease of obtaining a personal loan could tempt you into stretching your resources beyond their limit and living outside your means. To avoid this scenario, make sure you only take out a personal loan for a need or a high-value want, and make sure you can actually meet the repayment terms before you sign on the dotted line.

- Impacts your credit - Taking out a personal loan without any concomitant increase in your income will raise your debt-to-income ratio and, consequently, lower your credit score, making you seem less creditworthy to future lenders. Therefore, consider your potential future needs before taking out a personal loan in the present. If, for example, you think you may want to refinance your home or move to a new home in the near future, consider how a personal loan may impact your ability to do so.

Comparing Personal Loans

As you now understand, not all personal loans are built alike. Therefore, if you decide to pursue a personal loan for yourself, you need to look at what are the personal loans best for you.

When comparing different personal loans, examine these key criteria:

- Interest - What interest rate will each loan offer you? Often, you can submit a request for pre-qualification or pre-approval to get an idea of what a lender may offer you without impacting your credit score. Generally speaking, the lower the interest rate, the less you'll pay overall for the loan.

- Term - How long do you have to pay off each loan? While the longer you take to pay off a loan, the more you'll pay in interest for that benefit, the length of time you take to pay off a loan also impacts the size of your monthly payments. Make sure you find a loan with a payment schedule you can realistically and reasonably afford, lest you find yourself needing to take out a second personal loan to pay off the first, or risk default.

- Fees - Remember that your interest rate isn't the only cost involved in getting a personal loan. There may be ongoing origination fees or administrative fees, and the terms of the loan could allow for late fees if you miss your monthly payment and prepayment penalties if you pay back the full loan with interest before the end of its term.

- Time to Funding - How fast does each lender take to process your personal loan application and get the funds in your hands? Depending on how urgently you need the money, this can be a pressing factor.

- Options - Some lenders offer different options to make your borrowing and repayment experience easier, such as scheduled automatic withdrawals from your checking account or access to a secure online portal to track and manage your loan. Other lenders may give you a better interest rate if you already have a relationship with them, such as being a member of the credit union issuing you the loan.

Summary and Resources

A personal loan can be a powerful tool to help you weather a storm or improve your quality of life.

To make a personal loan work right for you, however, it requires a careful consideration of the advantages and drawbacks, both of personal loans in general and the specific personal loans you're considering.

To explore the personal loan options available to you in Jacksonville, Florida and the surrounding parts of Northern Florida, speak with one of our knowledgeable and friendly loan representatives at 121 Financial Credit Union.

He or she can even show you estimated rates you may qualify for with no affect to your credit score.

Visit us us at 121FCU.org or call us at 800-342-2352.